Chapter 17: Panel Data

17 Panel Data

17.1 Introduction

Economists traditionally use the term panel data to refer to data structures consisting of observations on individuals for multiple time periods. Other fields such as statistics typically call this structure longitudinal data. The observed “individuals” can be, for example, people, households, workers, firms, schools, production plants, industries, regions, states, or countries. The distinguishing feature relative to cross-sectional data sets is the presence of multiple observations for each individual. More broadly, panel data methods can be applied to any context with cluster-type dependence.

There are several distinct advantages of panel data relative to cross-section data. One is the possibility of controlling for unobserved time-invariant endogeneity without the use of instrumental variables. A second is the possibility of allowing for broader forms of heterogeneity. A third is modeling dynamic relationships and effects.

There are two broad categories of panel data sets in economic applications: micro panels and macro panels. Micro panels are typically surveys or administrative records on individuals and are characterized by a large number of individuals (often in the 1000’s or higher) and a relatively small number of time periods (often 2 to 20 years). Macro panels are typically national or regional macroeconomic variables and are characterized by a moderate number of individuals (e.g. 7-20) countries) is much less compelling (20-60 years).

Panel data was once relatively esoteric in applied economic practice. Now, it is a dominant feature of applied research.

A typical maintained assumption for micro panels (which we follow in this chapter) is that the individuals are mutually independent while the observations for a given individual are correlated across time periods. This means that the observations follow a clustered dependence structure. Because of this, current econometric practice is to use cluster-robust covariance matrix estimators when possible. Similar assumptions are often used for macro panels though the assumption of independence across individuals (e.g. countries) is much less compelling.

The application of panel data methods in econometrics started with the pioneering work of Mundlak (1961) and Balestra and Nerlove (1966).

Several excellent monographs and textbooks have been written on panel econometrics, including Arellano (2003), Hsiao (2003), Wooldridge (2010), and Baltagi (2013). This chapter will summarize some of the main themes but for a more in-depth treatment see these references.

One challenge arising in panel data applications is that the computational methods can require meticulous attention to detail. It is therefore advised to use established packages for routine applications. For most panel data applications in economics Stata is the standard package.

17.2 Time Indexing and Unbalanced Panels

It is typical to index observations by both the individual \(i\) and the time period \(t\), thus \(Y_{i t}\) denotes a variable for individual \(i\) in period \(t\). We index individuals as \(i=1, \ldots, N\) and time periods as \(t=1, \ldots T\). Thus \(N\) is the number of individuals in the panel and \(T\) is the number of time series periods.

Panel data sets can involve data at any time series frequency though the typical application involves annual data. The observations in a data set will be indexed by calendar time which for the case of annual observations is the year. For notational convenience it is customary to denote the time periods as \(t=\) \(1, \ldots, T\), so that \(t=1\) is the first time period observed and \(T\) is the final time period.

When observations are available on all individuals for the same time periods we say that the panel is balanced. In this case there are an equal number \(T\) of observations for each individual and the total number of observations is \(n=N T\).

When different time periods are available for the individuals in the sample we say that the panel is unbalanced. This is the most common type of panel data set. It does not pose a problem for applications but does make the notation cumbersome and also complicates computer programming.

To illustrate, consider the data set Invest 1993 on the textbook webpage. This is a sample of 1962 U.S. firms extracted from Compustat, assembled by Bronwyn Hall, and used in the empirical work in Hall and Hall (1993). In Table 17.1 we display a set of variables from the data set for the first 13 observations. The first variable is the firm code number. The second variable is the year of the observation. These two variables are essential for any panel data analysis. In Table \(17.1\) you can see that the first firm (#32) is observed for the years 1970 through 1977. The second firm (#209) is observed for 1987 through 1991. You can see that the years vary considerably across the firms so this is an unbalanced panel.

For unbalanced panels the time index \(t=1, \ldots, T\) denotes the full set of time periods. For example, in the data set Invest 1993 there are observations for the years 1960 through 1991, so the total number of time periods is \(T=32\). Each individual is observed for a subset of \(T_{i}\) periods. The set of time periods for individual \(i\) is denoted as \(S_{i}\) so that individual-specific sums (over time periods) are written as \(\sum_{t \in S_{i}}\).

The observed time periods for a given individual are typically contiguous (for example, in Table 17.1, firm #32 is observed for each year from 1970 through 1977) but in some cases are non-continguous (if, for example, 1973 was missing for firm #32). The total number of observations in the sample is \(n=\sum_{i=1}^{N} T_{i}\).

Table 17.1: Observations from Investment Data Set

| Firm Code Number | Year | \(I_{i t}\) | \(\bar{I}_{i}\) | \(\dot{I}_{i t}\) | \(Q_{i t}\) | \(\bar{Q}_{i}\) | \(\dot{Q}_{i t}\) | \(\widehat{e}_{i t}\) |

|---|---|---|---|---|---|---|---|---|

| 32 | 1970 | \(0.122\) | \(0.155\) | \(-0.033\) | \(1.17\) | \(0.62\) | \(0.55\) | . |

| 32 | 1971 | \(0.092\) | \(0.155\) | \(-0.063\) | \(0.79\) | \(0.62\) | \(0.17\) | \(-0.005\) |

| 32 | 1972 | \(0.094\) | \(0.155\) | \(-0.061\) | \(0.91\) | \(0.62\) | \(0.29\) | \(-0.005\) |

| 32 | 1973 | \(0.116\) | \(0.155\) | \(-0.039\) | \(0.29\) | \(0.62\) | \(-0.33\) | \(0.014\) |

| 32 | 1974 | \(0.099\) | \(0.155\) | \(-0.057\) | \(0.30\) | \(0.62\) | \(-0.32\) | \(-0.002\) |

| 32 | 1975 | \(0.187\) | \(0.155\) | \(0.032\) | \(0.56\) | \(0.62\) | \(-0.06\) | \(0.086\) |

| 32 | 1976 | \(0.349\) | \(0.155\) | \(0.194\) | \(0.38\) | \(0.62\) | \(-0.24\) | \(0.248\) |

| 32 | 1977 | \(0.182\) | \(0.155\) | \(0.027\) | \(0.57\) | \(0.62\) | \(-0.05\) | \(0.081\) |

| 209 | 1987 | \(0.095\) | \(0.071\) | \(0.024\) | \(9.06\) | \(21.57\) | \(-12.51\) | . |

| 209 | 1988 | \(0.044\) | \(0.071\) | \(-0.027\) | \(16.90\) | \(21.57\) | \(-4.67\) | \(-0.244\) |

| 209 | 1989 | \(0.069\) | \(0.071\) | \(-0.002\) | \(25.14\) | \(21.57\) | \(3.57\) | \(-0.257\) |

| 209 | 1990 | \(0.113\) | \(0.071\) | \(0.042\) | \(25.60\) | \(21.57\) | \(4.03\) | \(-0.226\) |

| 209 | 1991 | \(0.034\) | \(0.071\) | \(-0.037\) | \(31.14\) | \(21.57\) | \(9.57\) | \(-0.283\) |

17.3 Notation

This chapter focuses on panel data regression models whose observations are pairs \(\left(Y_{i t}, X_{i t}\right)\) where \(Y_{i t}\) is the dependent variable and \(X_{i t}\) is a \(k\)-vector of regressors. These are the observations on individual \(i\) for time period \(t\).

It will be useful to cluster the observations at the level of the individual. We borrow the notation from Section \(4.21\) to write \(\boldsymbol{Y}_{i}\) as the \(T_{i} \times 1\) stacked observations on \(Y_{i t}\) for \(t \in S_{i}\), stacked in chronological order. Similarly, we write \(\boldsymbol{X}_{i}\) as the \(T_{i} \times k\) matrix of stacked \(X_{i t}^{\prime}\) for \(t \in S_{i}\), stacked in chronological order.

We will also sometimes use matrix notation for the full sample. To do so, let \(\boldsymbol{Y}=\left(\boldsymbol{Y}_{1}^{\prime}, \ldots, \boldsymbol{Y}_{N}^{\prime}\right)^{\prime}\) denote the \(n \times 1\) vector of stacked \(\boldsymbol{Y}_{i}\), and set \(\boldsymbol{X}=\left(\boldsymbol{X}_{1}^{\prime}, \ldots, \boldsymbol{X}_{N}^{\prime}\right)^{\prime}\) similarly.

17.4 Pooled Regression

The simplest model in panel regresion is pooled regresssion

\[ \begin{aligned} Y_{i t} &=X_{i t}^{\prime} \beta+e_{i t} \\ \mathbb{E}\left[X_{i t} e_{i t}\right] &=0 . \end{aligned} \]

where \(\beta\) is a \(k \times 1\) coefficient vector and \(e_{i t}\) is an error. The model can be written at the level of the individual as

\[ \begin{aligned} \boldsymbol{Y}_{i} &=\boldsymbol{X}_{i} \beta+\boldsymbol{e}_{i} \\ \mathbb{E}\left[\boldsymbol{X}_{i}^{\prime} \boldsymbol{e}_{i}\right] &=0 \end{aligned} \]

where \(\boldsymbol{e}_{i}\) is \(T_{i} \times 1\). The equation for the full sample is \(\boldsymbol{Y}=\boldsymbol{X} \beta+\boldsymbol{e}\) where \(\boldsymbol{e}\) is \(n \times 1\).

The standard estimator of \(\beta\) in the pooled regression model is least squares, which can be written as

\[ \begin{aligned} \widehat{\beta}_{\text {pool }} &=\left(\sum_{i=1}^{N} \sum_{t \in S_{i}} X_{i t} X_{i t}^{\prime}\right)^{-1}\left(\sum_{i=1}^{N} \sum_{t \in S_{i}} X_{i t} Y_{i t}\right) \\ &=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{Y}_{i}\right) \\ &=\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1}\left(\boldsymbol{X}^{\prime} \boldsymbol{Y}\right) . \end{aligned} \]

In the context of panel data \(\widehat{\beta}_{\text {pool }}\) is called the pooled regression estimator. The vector of residuals for the \(i^{t h}\) individual is \(\widehat{\boldsymbol{e}}_{i}=\boldsymbol{Y}_{i}-\boldsymbol{X}_{i} \widehat{\beta}_{\text {pool }}\).

The pooled regression model is ideally suited for the context where the errors \(e_{i t}\) satisfy strict mean independence:

\[ \mathbb{E}\left[e_{i t} \mid \boldsymbol{X}_{i}\right]=0 . \]

This occurs when the errors \(e_{i t}\) are mean independent of all regressors \(X_{i j}\) for all time periods \(j=1, \ldots, T\). Strict mean independence is stronger than pairwise mean independence \(\mathbb{E}\left[e_{i t} \mid X_{i t}\right]=0\) as well as projection (17.1). Strict mean independence requires that neither lagged nor future values of \(X_{i t}\) help to forecast \(e_{i t}\). It excludes lagged dependent variables (such as \(Y_{i t-1}\) ) from \(X_{i t}\) (otherwise \(e_{i t}\) would be predictable given \(X_{i t+1}\) ). It also requires that \(X_{i t}\) is exogenous in the sense discussed in Chapter 12.

We now describe some statistical properties of \(\widehat{\beta}_{\text {pool }}\) under (17.2). First, notice that by linearity and the cluster-level notation we can write the estimator as

\[ \widehat{\beta}_{\mathrm{pool}}=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime}\left(\boldsymbol{X}_{i} \beta+\boldsymbol{e}_{i}\right)\right)=\beta+\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{e}_{i}\right) . \]

Using (17.2)

\[ \mathbb{E}\left[\widehat{\beta}_{\text {pool }} \mid \boldsymbol{X}\right]=\beta+\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \mathbb{E}\left[\boldsymbol{e}_{i} \mid \boldsymbol{X}_{i}\right]\right)=\beta \]

so \(\widehat{\beta}_{\text {pool }}\) is unbiased for \(\beta\).

Under the additional assumption that the error \(e_{i t}\) is serially uncorrelated and homoskedastic the covariance estimator takes a classical form and the classical homoskedastic variance estimator can be used. If the error \(e_{i t}\) is heteroskedastic but serially uncorrelated then a heteroskedasticity-robust covariance matrix estimator can be used.

In general, however, we expect the errors \(e_{i t}\) to be correlated across time \(t\) for a given individual. This does not necessarily violate (17.2) but invalidates classical covariance matrix estimation. The conventional solution is to use a cluster-robust covariance matrix estimator which allows arbitrary withincluster dependence. Cluster-robust covariance matrix estimators for pooled regression equal

\[ \widehat{\boldsymbol{V}}_{\text {pool }}=\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \widehat{\boldsymbol{e}}_{i} \widehat{\boldsymbol{e}}_{i}^{\prime} \boldsymbol{X}_{i}\right)\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1} . \]

As in (4.55) this can be multiplied by a degree-of-freedom adjustment. The adjustment used by the Stata regress command is

\[ \widehat{\boldsymbol{V}}_{\text {pool }}=\left(\frac{n-1}{n-k}\right)\left(\frac{N}{N-1}\right)\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \widehat{\boldsymbol{e}}_{i} \widehat{\boldsymbol{e}}_{i}^{\prime} \boldsymbol{X}_{i}\right)\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1} \]

The pooled regression estimator with cluster-robust standard errors can be obtained using the Stata command regress cluster(id) where id indicates the individual.

When strict mean independence (17.2) fails the pooled least squares estimator \(\widehat{\beta}_{\text {pool }}\) is not necessarily consistent for \(\beta\). Since strict mean independence is a strong and undesirable restriction it is typically preferred to adopt one of the alternative estimators described in the following sections.

To illustrate the pooled regression estimator consider the data set Invest1993 described earlier. We consider a simple investment model

\[ I_{i t}=\beta_{1} Q_{i t-1}+\beta_{2} D_{i t-1}+\beta_{3} C F_{i t-1}+\beta_{4} T_{i}+e_{i t} \]

where \(I\) is investment/assets, \(Q\) is market value/assets, \(D\) is long term debt/assets, \(C F\) is cash flow/assets, and \(T\) is a dummy variable indicating if the corporation’s stock is traded on the NYSE or AMEX. The regression also includes 19 dummy variables indicating an industry code. The \(Q\) theory of investment suggests that \(\beta_{1}>0\) while \(\beta_{2}=\beta_{3}=0\). Theories of liquidity constraints suggest that \(\beta_{2}<0\) and \(\beta_{3}>0\). We will be using this example throughout this chapter. The values of \(I\) and \(Q\) for the first 13 observations are also displayed in Table 17.1.

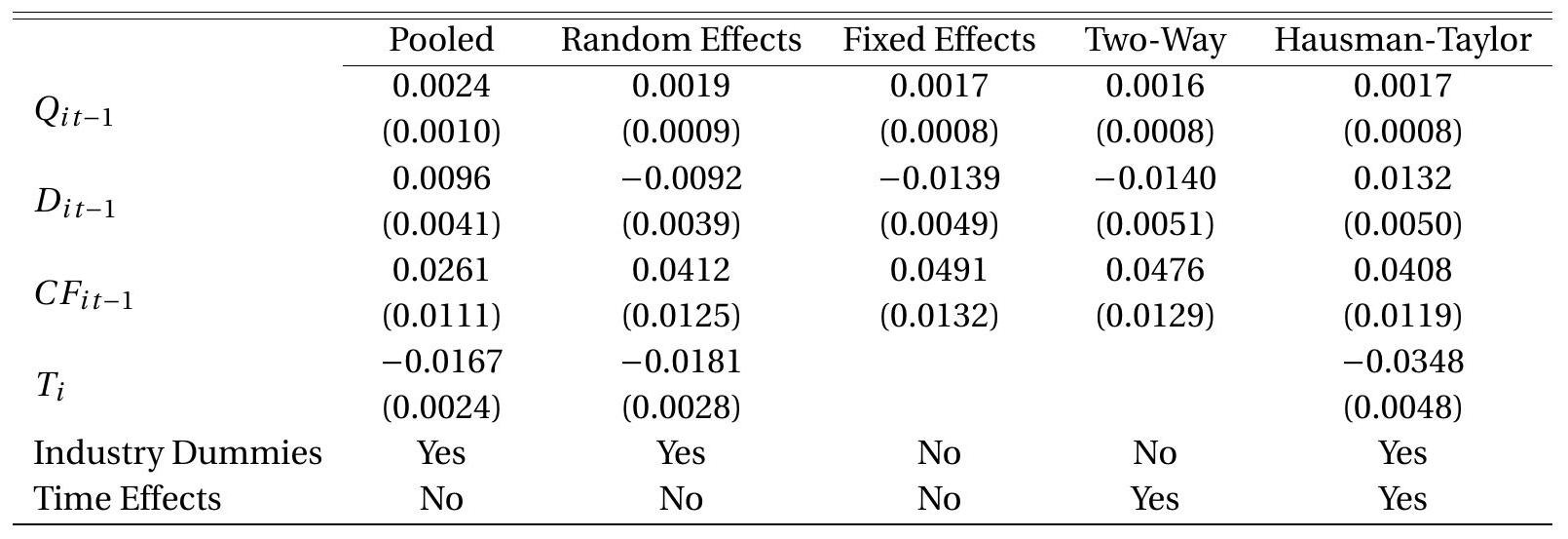

In Table \(17.2\) we present the pooled regression estimates of (17.3) in the first column with clusterrobust standard errors.

17.5 One-Way Error Component Model

One approach to panel data regression is to model the correlation structure of the regression error \(e_{i t}\). The most common choice is an error-components structure. The simplest takes the form

\[ e_{i t}=u_{i}+\varepsilon_{i t} \]

Table 17.2: Estimates of Investment Equation

Cluster-robust standard errors in parenthesis.

where \(u_{i}\) is an individual-specific effect and \(\varepsilon_{i t}\) are idiosyncratic (i.i.d.) errors. This is known as a oneway error component model.

In vector notation we can write \(\boldsymbol{e}_{i}=\mathbf{1}_{i} u_{i}+\boldsymbol{\varepsilon}_{i}\) where \(\mathbf{1}_{i}\) is a \(T_{i} \times 1\) vector of 1’s.

The one-way error component regression model is

\[ Y_{i t}=X_{i t}^{\prime} \beta+u_{i}+\varepsilon_{i t} \]

written at the level of the observation, or \(\boldsymbol{Y}_{i}=\boldsymbol{X}_{i} \beta+\mathbf{1}_{i} u_{i}+\boldsymbol{\varepsilon}_{i}\) written at the level of the individual.

To illustrate why an error-component structure such as (17.4) might be appropriate, examine Table 17.1. In the final column we have included the pooled regression residuals \(\widehat{e}_{i t}\) for these observations. (There is no residual for the first year for each firm due to the lack of lagged regressors for this observation.) What is quite striking is that the residuals for the second firm (#209) are all negative, clustering around \(-0.25\). While informal, this suggests that it may be appropriate to model these errors using (17.4), expecting that firm #209 has a large negative value for its individual effect \(u\).

17.6 Random Effects

The random effects model assumes that the errors \(u_{i}\) and \(\varepsilon_{i t}\) in (17.4) are conditionally mean zero, uncorrelated, and homoskedastic.

Assumption 17.1 Random Effects. Model (17.4) holds with

\[ \begin{aligned} \mathbb{E}\left[\varepsilon_{i t} \mid \boldsymbol{X}_{i}\right] &=0 \\ \mathbb{E}\left[\varepsilon_{i t}^{2} \mid \boldsymbol{X}_{i}\right] &=\sigma_{\varepsilon}^{2} \\ \mathbb{E}\left[\varepsilon_{i t} \varepsilon_{j s} \mid \boldsymbol{X}_{i}\right] &=0 \\ \mathbb{E}\left[u_{i} \mid \boldsymbol{X}_{i}\right] &=0 \\ \mathbb{E}\left[u_{i}^{2} \mid \boldsymbol{X}_{i}\right] &=\sigma_{u}^{2} \\ \mathbb{E}\left[u_{i} \varepsilon_{i t} \mid \boldsymbol{X}_{i}\right] &=0 \end{aligned} \]

where (17.7) holds for all \(s \neq t\). Assumption \(17.1\) is known as a random effects specification. It implies that the vector of errors \(\boldsymbol{e}_{i}\) for individual \(i\) has the covariance structure

\[ \begin{aligned} \mathbb{E}\left[\boldsymbol{e}_{i} \mid \boldsymbol{X}_{i}\right] &=0 \\ \mathbb{E}\left[\boldsymbol{e}_{i} \boldsymbol{e}_{i}^{\prime} \mid \boldsymbol{X}_{i}\right] &=\mathbf{1}_{i} \mathbf{1}_{i}^{\prime} \sigma_{u}^{2}+\boldsymbol{I}_{i} \sigma_{\varepsilon}^{2} \\ &=\left(\begin{array}{cccc} \sigma_{u}^{2}+\sigma_{\varepsilon}^{2} & \sigma_{u}^{2} & \cdots & \sigma_{u}^{2} \\ \sigma_{u}^{2} & \sigma_{u}^{2}+\sigma_{\varepsilon}^{2} & \cdots & \sigma_{u}^{2} \\ \vdots & \vdots & \ddots & \vdots \\ \sigma_{u}^{2} & \sigma_{u}^{2} & \cdots & \sigma_{u}^{2}+\sigma_{\varepsilon}^{2} \end{array}\right) \\ &=\sigma_{\varepsilon}^{2} \Omega_{i}, \end{aligned} \]

say, where \(\boldsymbol{I}_{i}\) is an identity matrix of dimension \(T_{i}\). The matrix \(\Omega_{i}\) depends on \(i\) since its dimension depends on the number of observed time periods \(T_{i}\).

Assumptions 17.1.1 and 17.1.4 state that the idiosyncratic error \(\varepsilon_{i t}\) and individual-specific error \(u_{i}\) are strictly mean independent so the combined error \(e_{i t}\) is strictly mean independent as well.

The random effects model is equivalent to an equi-correlation model. That is, suppose that the error \(e_{i t}\) satisfies

\[ \begin{aligned} \mathbb{E}\left[e_{i t} \mid \boldsymbol{X}_{i}\right] &=0 \\ \mathbb{E}\left[e_{i t}^{2} \mid \boldsymbol{X}_{i}\right] &=\sigma^{2} \end{aligned} \]

and

\[ \mathbb{E}\left[e_{i s} e_{i t} \mid \boldsymbol{X}_{i}\right]=\rho \sigma^{2} \]

for \(s \neq t\). These conditions imply that \(e_{i t}\) can be written as (17.4) with the components satisfying Assumption \(17.1\) with \(\sigma_{u}^{2}=\rho \sigma^{2}\) and \(\sigma_{\varepsilon}^{2}=(1-\rho) \sigma^{2}\). Thus random effects and equi-correlation are identical.

The random effects regression model is

\[ Y_{i t}=X_{i t}^{\prime} \beta+u_{i}+\varepsilon_{i t} \]

or \(\boldsymbol{Y}_{i}=\boldsymbol{X}_{i} \beta+\mathbf{1}_{i} u_{i}+\boldsymbol{\varepsilon}_{i}\) where the errors satisfy Assumption 17.1.

Given the error structure the natural estimator for \(\beta\) is GLS. Suppose \(\sigma_{u}^{2}\) and \(\sigma_{\varepsilon}^{2}\) are known. The GLS estimator of \(\beta\) is

\[ \widehat{\beta}_{\mathrm{gls}}=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{Y}_{i}\right) . \]

A feasible GLS estimator replaces the unknown \(\sigma_{u}^{2}\) and \(\sigma_{\varepsilon}^{2}\) with estimators. See Section \(17.15\).

We now describe some statistical properties of the estimator under Assumption 17.1. By linearity

\[ \widehat{\beta}_{\mathrm{gls}}-\beta=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{e}_{i}\right) . \]

Thus

\[ \mathbb{E}\left[\widehat{\beta}_{\mathrm{gls}}-\beta \mid \boldsymbol{X}\right]=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \mathbb{E}\left[\boldsymbol{e}_{i} \mid \boldsymbol{X}_{i}\right]\right)=0 . \]

Thus \(\widehat{\beta}_{\text {gls }}\) is conditionally unbiased for \(\beta\). The conditional variance of \(\widehat{\beta}_{\text {gls }}\) is

\[ \boldsymbol{V}_{\mathrm{gls}}=\left(\sum_{i=1}^{n} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)^{-1} \sigma_{\varepsilon}^{2} \]

Now let’s compare \(\widehat{\beta}_{\text {gls }}\) with the pooled estimator \(\widehat{\beta}_{\text {pool. }}\). Under Assumption \(17.1\) the latter is also conditionally unbiased for \(\beta\) and has conditional variance

\[ \boldsymbol{V}_{\text {pool }}=\left(\sum_{i=1}^{n} \boldsymbol{X}_{i}^{\prime} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{n} \boldsymbol{X}_{i}^{\prime} \Omega_{i} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{n} \boldsymbol{X}_{i}^{\prime} \boldsymbol{X}_{i}\right)^{-1} . \]

Using the algebra of the Gauss-Markov Theorem we deduce that

\[ \boldsymbol{V}_{\text {gls }} \leq \boldsymbol{V}_{\text {pool }} \]

and thus the random effects estimator \(\widehat{\beta}_{\text {gls }}\) is more efficient than the pooled estimator \(\widehat{\beta}_{\text {pool }}\) under Assumption 17.1. (See Exercise 17.1.) The two variance matrices are identical when there is no individualspecific effect (when \(\sigma_{u}^{2}=0\) ) for then \(\boldsymbol{V}_{\text {gls }}=\boldsymbol{V}_{\text {pool }}=\left(\boldsymbol{X}^{\prime} \boldsymbol{X}\right)^{-1} \sigma_{\varepsilon}^{2}\).

Under the assumption that the random effects model is a useful approximation but not literally true then we may consider a cluster-robust covariance matrix estimator such as

\[ \widehat{\boldsymbol{V}}_{\mathrm{gls}}=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \widehat{\boldsymbol{e}}_{i} \widehat{\boldsymbol{e}}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)\left(\sum_{i=1}^{n} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)^{-1} \]

where \(\widehat{\boldsymbol{e}}_{i}=\boldsymbol{Y}_{i}-\boldsymbol{X}_{i} \widehat{\beta}_{\mathrm{gls}}\). This may be re-scaled by a degree of freedom adjustment if desired.

The random effects estimator \(\widehat{\beta}_{\text {gls }}\) can be obtained using the Stata command xtreg. The default covariance matrix estimator is (17.11). For the cluster-robust covariance matrix estimator (17.14) use the command xtreg vce(robust). (The xtset command must be used first to declare the group identifier. For example, cusip is the group identifier in Table 17.1.)

To illustrate, in the second column of Table \(17.2\) we present the random effect regression estimates of the investment model (17.3) with cluster-robust standard errors (17.14). The point estimates are reasonably different from the pooled regression estimator. The coefficient on debt switches from positive to negative (the latter consistent with theories of liquidity constraints) and the coefficient on cash flow increases significantly in magnitude. These changes appear to be greater in magnitude than would be expected if Assumption \(17.1\) were correct. In the next section we consider a less restrictive specification.

17.7 Fixed Effect Model

Consider the one-way error component regression model

\[ Y_{i t}=X_{i t}^{\prime} \beta+u_{i}+\varepsilon_{i t} \]

or

\[ \boldsymbol{Y}_{i}=\boldsymbol{X}_{i} \beta+\mathbf{l}_{i} u_{i}+\boldsymbol{\varepsilon}_{i} . \]

In many applications it is useful to interpret the individual-specific effect \(u_{i}\) as a time-invariant unobserved missing variable. For example, in a wage regression \(u_{i}\) may be the unobserved ability of individual \(i\). In the investment model (17.3) \(u_{i}\) may be a firm-specific productivity factor.

When \(u_{i}\) is interpreted as an omitted variable it is natural to expect it to be correlated with the regressors \(X_{i t}\). This is especially the case when \(X_{i t}\) includes choice variables.

To illustrate, consider the entries in Table 17.1. The final column displays the pooled regression residuals \(\widehat{e}_{i t}\) for the first 13 observations which we interpret as estimates of the error \(e_{i t}=u_{i}+\varepsilon_{i t}\). As described before, what is particularly striking about the residuals is that they are all strongly negative for firm #209, clustering around \(-0.25\). We can interpret this as an estimate of \(u_{i}\) for this firm. Examining the values of the regressor \(Q\) for the two firms we can see that firm #209 has very large values (in all time periods) for \(Q\). (The average value \(\bar{Q}_{i}\) for the two firms appears in the seventh column.) Thus it appears (though we are only looking at two observations) that \(u_{i}\) and \(Q_{i t}\) are correlated. It is not reasonable to infer too much from these limited observations, but the relevance is that such correlation violates strict mean independence.

In the econometrics literature if the stochastic structure of \(u_{i}\) is treated as unknown and possibly correlated with \(X_{i t}\) then \(u_{i}\) is called a fixed effect.

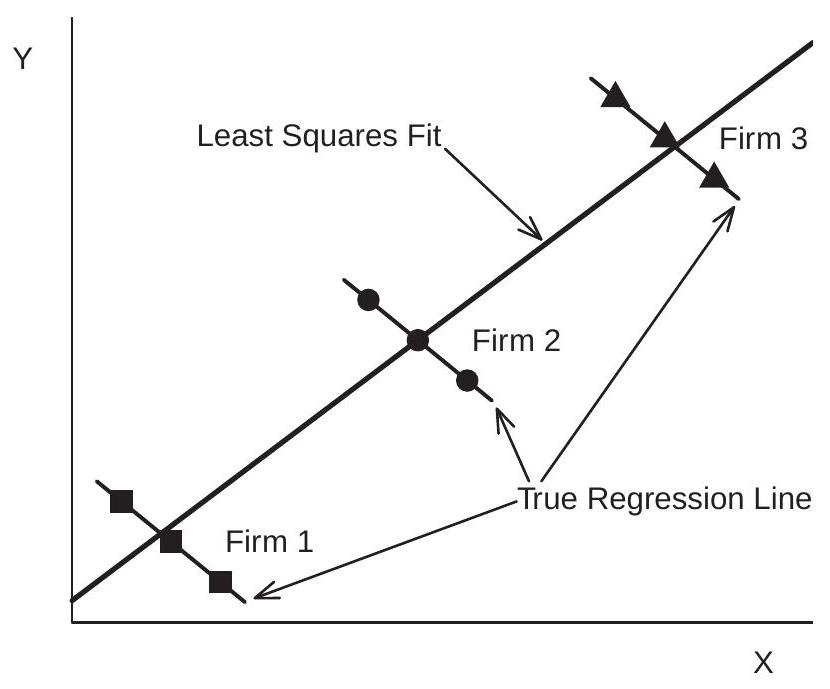

Correlation between \(u_{i}\) and \(X_{i t}\) will cause both pooled and random effect estimators to be biased. This is due to the classic problems of omitted variables bias and endogeneity. To see this in a generated example view Figure 17.1. This shows a scatter plot of three observations \(\left(Y_{i t}, X_{i t}\right)\) from three firms. The true model is \(Y_{i t}=9-X_{i t}+u_{i}\). (The true slope coefficient is \(-1\).) The variables \(u_{i}\) and \(X_{i t}\) are highly correlated so the fitted pooled regression line through the nine observations has a slope close to +1. (The random effects estimator is identical.) The apparent positive relationship between \(Y\) and \(X\) is driven entirely by the positive correlation between \(X\) and \(u\). Conditional on \(u\), however, the slope is \(-1\). Thus regression techniques which do not control for \(u_{i}\) will produce biased and inconsistent estimators.

Figure 17.1: Scatter Plot and Pooled Regression Line

The presence of the unstructured individual effect \(u_{i}\) means that it is not possible to identify \(\beta\) under a simple projection assumption such as \(\mathbb{E}\left[X_{i t} \varepsilon_{t}\right]=0\). It turns out that a sufficient condition for identification is the following. Definition 17.1 The regressor \(X_{i t}\) is strictly exogenous for the error \(\varepsilon_{i t}\) if

\[ \mathbb{E}\left[X_{i s} \varepsilon_{i t}\right]=0 \]

for all \(s=1, \ldots, T\).

Strict exogeneity is a strong projection condition, meaning that if \(X_{i s}\) for any \(s \neq t\) is added to (17.15) it will have a zero coefficient. Strict exogeneity is a projection analog of strict mean independence

\[ \mathbb{E}\left[\varepsilon_{i t} \mid \boldsymbol{X}_{i}\right]=0 . \]

(17.18) implies (17.17) but not conversely. While (17.17) is sufficient for identification and asymptotic theory we will also use the stronger condition (17.18) for finite sample analysis.

While (17.17) and (17.18) are strong assumptions they are much weaker than (17.2) or Assumption 17.1, which require that the individual effect \(u_{i}\) is also strictly mean independent. In contrast, (17.17) and (17.18) make no assumptions about \(u_{i}\).

Strict exogeneity (17.17) is typically inappropriate in dynamic models. In Section \(17.41\) we discuss estimation under the weaker assumption of predetermined regressors.

17.8 Within Transformation

In the previous section we showed that if \(u_{i}\) and \(X_{i t}\) are correlated then pooled and random-effects estimators will be biased and inconsistent. If we leave the relationship between \(u_{i}\) and \(X_{i t}\) fully unstructured then the only way to consistently estimate the coefficient \(\beta\) is by an estimator which is invariant to \(u_{i}\). This can be achieved by transformations which eliminate \(u_{i}\).

One such transformation is the within transformation. In this section we describe this transformation in detail.

Define the mean of a variable for a given individual as

\[ \bar{Y}_{i}=\frac{1}{T_{i}} \sum_{t \in S_{i}} Y_{i t} . \]

We call this the individual-specific mean since it is the mean of a given individual. Contrarywise, some authors call this the time-average or time-mean since it is the average over the time periods.

Subtracting the individual-specific mean from the variable we obtain the deviations

\[ \dot{Y}_{i t}=Y_{i t}-\bar{Y}_{i} . \]

This is known as the within transformation. We also refer to \(\dot{Y}_{i t}\) as the demeaned values or deviations from individual means. Some authors refer to \(\dot{Y}_{i t}\) as deviations from time means. What is important is that the demeaning has occured at the individual level.

Some algebra may also be useful. We can write the individual-specific mean as \(\bar{Y}_{i}=\left(\mathbf{1}_{i}^{\prime} \mathbf{1}_{i}\right)^{-1} \mathbf{1}_{i}^{\prime} \boldsymbol{Y}_{i}\). Stacking the observations for individual \(i\) we can write the within transformation using the notation

\[ \begin{aligned} \dot{\boldsymbol{Y}}_{i} &=\boldsymbol{Y}_{i}-\mathbf{1}_{i} \bar{Y}_{i} \\ &=\boldsymbol{Y}_{i}-\mathbf{1}_{i}\left(\mathbf{1}_{i}^{\prime} \mathbf{1}_{i}\right)^{-1} \mathbf{1}_{i}^{\prime} \boldsymbol{Y}_{i} \\ &=\boldsymbol{M}_{i} \boldsymbol{Y}_{i} \end{aligned} \]

where \(\boldsymbol{M}_{i}=\boldsymbol{I}_{i}-\mathbf{1}_{i}\left(\mathbf{1}_{i}^{\prime} \mathbf{1}_{i}\right)^{-1} \mathbf{1}_{i}^{\prime}\) is the individual-specific demeaning operator. Notice that \(\boldsymbol{M}_{i}\) is an idempotent matrix.

Similarly for the regressors we define the individual-specific means and demeaned values:

\[ \begin{aligned} \bar{X}_{i} &=\frac{1}{T_{i}} \sum_{t \in S_{i}} X_{i t} \\ \dot{X}_{i t} &=X_{i t}-\bar{X}_{i} \\ \dot{\boldsymbol{X}}_{i} &=\boldsymbol{M}_{i} \boldsymbol{X}_{i} . \end{aligned} \]

We illustrate demeaning in Table 17.1. In the fourth and seventh columns we display the firm-specific means \(\bar{I}_{i}\) and \(\bar{Q}_{i}\) and in the fifth and eighth columns the demeaned values \(\dot{I}_{i t}\) and \(\dot{Q}_{i t}\).

We can also define the full-sample within operator. Define \(\boldsymbol{D}=\operatorname{diag}\left\{\mathbf{1}_{T_{1}}, \ldots, \mathbf{1}_{T_{N}}\right\}\) and \(\boldsymbol{M}_{\boldsymbol{D}}=\boldsymbol{I}_{n}-\) \(\boldsymbol{D}\left(\boldsymbol{D}^{\prime} \boldsymbol{D}\right)^{-1} \boldsymbol{D}^{\prime}\). Note that \(\boldsymbol{M}_{\boldsymbol{D}}=\operatorname{diag}\left\{\boldsymbol{M}_{1}, \ldots, \boldsymbol{M}_{N}\right\}\). Thus

\[ \boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{Y}=\dot{\boldsymbol{Y}}=\left(\begin{array}{c} \dot{\boldsymbol{Y}}_{1} \\ \vdots \\ \dot{\boldsymbol{Y}}_{N} \end{array}\right), \quad \boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{X}=\dot{\boldsymbol{X}}=\left(\begin{array}{c} \dot{\boldsymbol{X}}_{1} \\ \vdots \\ \dot{\boldsymbol{X}}_{N} \end{array}\right) \]

Now apply these operations to equation (17.15). Taking individual-specific averages we obtain

\[ \bar{Y}_{i}=\bar{X}_{i}^{\prime} \beta+u_{i}+\bar{\varepsilon}_{i} \]

where \(\bar{\varepsilon}_{i}=\frac{1}{T_{i}} \sum_{t \in S_{i}} \varepsilon_{i t}\). Subtracting from (17.15) we obtain

\[ \dot{Y}_{i t}=\dot{X}_{i t}^{\prime} \beta+\dot{\varepsilon}_{i t} \]

where \(\dot{\varepsilon}_{i t}=\varepsilon_{i t}-\bar{\varepsilon}_{i t}\). The individual effect \(u_{i}\) has been eliminated! obtain

We can alternatively write this in vector notation. Applying the demeaning operator \(\boldsymbol{M}_{i}\) to (17.16) we

\[ \dot{\boldsymbol{Y}}_{i}=\dot{\boldsymbol{X}}_{i} \beta+\dot{\boldsymbol{\varepsilon}}_{i} . \]

The individual-effect \(u_{i}\) is eliminated because \(\boldsymbol{M}_{i} \mathbf{1}_{i}=0\). Equation (17.22) is a vector version of (17.21).

The equation (17.21) is a linear equation in the transformed (demeaned) variables. As desired the individual effect \(u_{i}\) has been eliminated. Consequently estimators constructed from (17.21) (or equivalently (17.22)) will be invariant to the values of \(u_{i}\). This means that the the endogeneity bias described in the previous section will be eliminated.

Another consequence, however, is that all time-invariant regressors are also eliminated. That is, if the original model (17.15) had included any regressors \(X_{i t}=X_{i}\) which are constant over time for each individual then for these regressors the demeaned values are identically 0 . What this means is that if equation (17.21) is used to estimate \(\beta\) it will be impossible to estimate (or identify) a coefficient on any regressor which is time invariant. This is not a consequence of the estimation method but rather a consequence of the model assumptions. In other words, if the individual effect \(u_{i}\) has no known structure then it is impossible to disentangle the effect of any time-invariant regressor \(X_{i}\). The two have observationally equivalent effects and cannot be separately identified.

The within transformation can greatly reduce the variance of the regressors. This can be seen in Table 17.1 where you can see that the variation between the elements of the transformed variables \(\dot{I}_{i t}\) and \(\dot{Q}_{i t}\) is less than that of the untransformed variables, as much of the variation is captured by the firm-specific means.

It is not typically needed to directly program the within transformation, but if it is desired the following Stata commands easily do so.

| Stata Commands for Within Transformation |

|---|

| \(* \quad \quad \mathrm{x}\) is the original variable |

| \(* \quad\) id is the group identifier |

| \(* \quad\) xdot is the within-transformed variable |

| egen xmean \(=\) mean \((\mathrm{x})\), by(id) gen xdot \(=\mathrm{x}-\mathrm{xmean}\) |

17.9 Fixed Effects Estimator

Consider least squares applied to the demeaned equation (17.21) or equivalently (17.22). This is

\[ \begin{aligned} \widehat{\beta}_{\mathrm{fe}} &=\left(\sum_{i=1}^{N} \sum_{t \in S_{i}} \dot{X}_{i t} \dot{X}_{i t}^{\prime}\right)^{-1}\left(\sum_{i=1}^{N} \sum_{t \in S_{i}} \dot{X}_{i t} \dot{Y}_{i t}\right) \\ &=\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \dot{\boldsymbol{Y}}_{i}\right) \\ &=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \boldsymbol{Y}_{i}\right) \end{aligned} \]

This is known as the fixed-effects or within estimator of \(\beta\). It is called the fixed-effects estimator because it is appropriate for the fixed effects model (17.15). It is called the within estimator because it is based on the variation of the data within each individual.

The above definition implicitly assumes that the matrix \(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\) is full rank. This requires that all components of \(X_{i t}\) have time variation for at least some individuals in the sample.

The fixed effects residuals are

\[ \begin{aligned} \widehat{\varepsilon}_{i t} &=\dot{Y}_{i t}-\dot{X}_{i t}^{\prime} \widehat{\beta}_{\mathrm{fe}} \\ \widehat{\boldsymbol{\varepsilon}}_{i} &=\dot{\boldsymbol{Y}}_{i}-\dot{\boldsymbol{X}}_{i} \widehat{\beta}_{\mathrm{fe}} \end{aligned} \]

Let us describe some of the statistical properties of the estimator under strict mean independence (17.18). By linearity and the fact \(\boldsymbol{M}_{i} \mathbf{1}_{i}=0\), we can write

\[ \widehat{\beta}_{\mathrm{fe}}-\beta=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \boldsymbol{\varepsilon}_{i}\right) \]

Then (17.18) implies

\[ \mathbb{E}\left[\widehat{\beta}_{\mathrm{fe}}-\beta \mid \boldsymbol{X}\right]=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \mathbb{E}\left[\boldsymbol{\varepsilon}_{i} \mid \boldsymbol{X}_{i}\right]\right)=0 \]

Thus \(\widehat{\beta}_{\mathrm{fe}}\) is unbiased for \(\beta\) under (17.18).

Let \(\Sigma_{i}=\mathbb{E}\left[\boldsymbol{\varepsilon}_{i} \boldsymbol{\varepsilon}_{i}^{\prime} \mid \boldsymbol{X}_{i}\right]\) denote the \(T_{i} \times T_{i}\) conditional covariance matrix of the idiosyncratic errors. The variance of \(\widehat{\beta}_{\mathrm{fe}}\) is

\[ \boldsymbol{V}_{\mathrm{fe}}=\operatorname{var}\left[\widehat{\beta}_{\mathrm{fe}} \mid \boldsymbol{X}\right]=\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \Sigma_{i} \dot{\boldsymbol{X}}_{i}\right)\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)^{-1} \]

This expression simplifies when the idiosyncratic errors are homoskedastic and serially uncorrelated:

\[ \begin{aligned} \mathbb{E}\left[\varepsilon_{i t}^{2} \mid \boldsymbol{X}_{i}\right] &=\sigma_{\varepsilon}^{2} \\ \mathbb{E}\left[\varepsilon_{i j} \varepsilon_{i t} \mid \boldsymbol{X}_{i}\right] &=0 \end{aligned} \]

for all \(j \neq t\). In this case, \(\Sigma_{i}=\boldsymbol{I}_{i} \sigma_{\varepsilon}^{2}\) and (17.24) simplifies to

\[ \boldsymbol{V}_{\mathrm{fe}}^{0}=\sigma_{\varepsilon}^{2}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)^{-1} . \]

It is instructive to compare the variances of the fixed-effects and pooled estimators under (17.25)(17.26) and the assumption that there is no individual-specific effect \(u_{i}=0\). In this case we see that

\[ \boldsymbol{V}_{\mathrm{fe}}^{0}=\sigma_{\varepsilon}^{2}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)^{-1} \geq \sigma_{\varepsilon}^{2}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{X}_{i}\right)^{-1}=\boldsymbol{V}_{\text {pool }} \]

The inequality holds since the demeaned variables \(\dot{\boldsymbol{X}}_{i}\) have reduced variation relative to the original observations \(\boldsymbol{X}_{i}\). (See Exercise 17.28.) This shows the cost of using fixed effects relative to pooled estimation. The estimation variance increases due to reduced variation in the regressors. This reduction in efficiency is a necessary by-product of the robustness of the estimator to the individual effects \(u_{i}\).

17.10 Differenced Estimator

The within transformation is not the only transformation which eliminates the individual-specific effect. Another important transformation which does the same is first-differencing.

The first-differencing transformation is \(\Delta Y_{i t}=Y_{i t}-Y_{i t-1}\). This can be applied to all but the first observation (which is essentially lost). At the level of the individual this can be written as \(\Delta \boldsymbol{Y}_{i}=\boldsymbol{D}_{i} \boldsymbol{Y}_{i}\) where \(\boldsymbol{D}_{i}\) is the \(\left(T_{i}-1\right) \times T_{i}\) matrix differencing operator

\[ \boldsymbol{D}_{i}=\left[\begin{array}{cccccc} -1 & 1 & 0 & \cdots & 0 & 0 \\ 0 & -1 & 1 & & 0 & 0 \\ \vdots & & & \ddots & & \vdots \\ 0 & 0 & 0 & \cdots & -1 & 1 \end{array}\right] . \]

Applying the transformation \(\Delta\) to (17.15) or (17.16) we obtain \(\Delta Y_{i t}=\Delta X_{i t}^{\prime} \beta+\Delta \varepsilon_{i t}\) or

\[ \Delta \boldsymbol{Y}_{i}=\Delta \boldsymbol{X}_{i} \beta+\Delta \boldsymbol{\varepsilon}_{i} . \]

We can see that the individual effect \(u_{i}\) has been eliminated.

Least squares applied to the differenced equation (17.29) is

\[ \begin{aligned} \widehat{\beta}_{\Delta} &=\left(\sum_{i=1}^{N} \sum_{t \geq 2} \Delta X_{i t} \Delta X_{i t}^{\prime}\right)^{-1}\left(\sum_{i=1}^{N} \sum_{t \geq 2} \Delta X_{i t} \Delta Y_{i t}\right) \\ &=\left(\sum_{i=1}^{N} \Delta \boldsymbol{X}_{i}^{\prime} \Delta \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \Delta \boldsymbol{X}_{i}^{\prime} \Delta \boldsymbol{Y}_{i}\right) \\ &=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{D}_{i}^{\prime} \boldsymbol{D}_{i} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{D}_{i}^{\prime} \boldsymbol{D}_{i} \boldsymbol{Y}_{i}\right) \end{aligned} \]

(17.30) is called the differenced estimator. For \(T=2, \widehat{\beta}_{\Delta}=\widehat{\beta}_{\mathrm{fe}}\) equals the fixed effects estimator. See Exercise 17.6. They differ, however, for \(T>2\).

When the errors \(\varepsilon_{i t}\) are serially uncorrelated and homoskedastic then the error \(\Delta \boldsymbol{\varepsilon}_{i}=\boldsymbol{D}_{i} \boldsymbol{\varepsilon}_{i}\) in (17.29) has covariance matrix \(\boldsymbol{H} \sigma_{\varepsilon}^{2}\) where

\[ \boldsymbol{H}=\boldsymbol{D}_{i} \boldsymbol{D}_{i}^{\prime}=\left(\begin{array}{cccc} 2 & -1 & 0 & 0 \\ -1 & 2 & \ddots & 0 \\ 0 & \ddots & \ddots & -1 \\ 0 & 0 & -1 & 2 \end{array}\right) . \]

We can reduce estimation variance by using GLS. When the errors \(\varepsilon_{i t}\) are i.i.d. (serially uncorrelated and homoskedastic), this is

\[ \begin{aligned} \widetilde{\beta}_{\Delta} &=\left(\sum_{i=1}^{N} \Delta \boldsymbol{X}_{i}^{\prime} \boldsymbol{H}^{-1} \Delta \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \Delta \boldsymbol{X}_{i}^{\prime} \boldsymbol{H}^{-1} \Delta \boldsymbol{Y}_{i}\right) \\ &=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{D}_{i}^{\prime}\left(\boldsymbol{D}_{i} \boldsymbol{D}_{i}^{\prime}\right)^{-1} \boldsymbol{D}_{i} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{D}_{i}^{\prime}\left(\boldsymbol{D}_{i} \boldsymbol{D}_{i}^{\prime}\right)^{-1} \boldsymbol{D}_{i} \boldsymbol{Y}_{i}\right) \\ &=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \boldsymbol{M}_{i} \boldsymbol{Y}_{i}\right) \end{aligned} \]

where \(\boldsymbol{M}_{i}=\boldsymbol{D}_{i}^{\prime}\left(\boldsymbol{D}_{i} \boldsymbol{D}_{i}^{\prime}\right)^{-1} \boldsymbol{D}_{i}\). Recall, the matrix \(\boldsymbol{D}_{i}\) is \(\left(T_{i}-1\right) \times T_{i}\) with rank \(T_{i}-1\) and is orthogonal to the vector of ones \(\mathbf{1}_{i}\). This means \(\boldsymbol{M}_{i}\) projects orthogonally to \(\mathbf{1}_{i}\) and thus equals the within transformation matrix. Hence \(\widetilde{\beta}_{\Delta}=\widehat{\beta}_{\mathrm{fe}}\), the fixed effects estimator!

What we have shown is that under i.i.d. errors, GLS applied to the first-differenced equation precisely equals the fixed effects estimator. Since the Gauss-Markov theorem shows that GLS has lower variance than least squares, this means that the fixed effects estimator is more efficient than first differencing under the assumption that \(\varepsilon_{i t}\) is i.i.d.

This argument extends to any other transformation which eliminates the fixed effect. GLS applied after such a transformation is equal to the fixed effects estimator and is more efficient than least squares applied after the same transformation under i.i.d. errors. This shows that the fixed effects estimator is Gauss-Markov efficient in the class of estimators which eliminate the fixed effect, under these assumptions.

17.11 Dummy Variables Regression

An alternative way to estimate the fixed effects model is by least squares of \(Y_{i t}\) on \(X_{i t}\) and a full set of dummy variables, one for each individual in the sample. It turns out that this is algebraically equivalent to the within estimator.

To see this start with the error-component model without a regressor:

\[ Y_{i t}=u_{i}+\varepsilon_{i t} . \]

Consider least squares estimation of the vector of fixed effects \(u=\left(u_{1}, \ldots, u_{N}\right)^{\prime}\). Since each fixed effect \(u_{i}\) is an individual-specific mean and the least squares estimate of the intercept is the sample mean it follows that the least squares estimate of \(u_{i}\) is \(\widehat{u}_{i}=\bar{Y}_{i}\). The least squares residual is then \(\widehat{\varepsilon}_{i t}=Y_{i t}-\bar{Y}_{i}=\) \(\dot{Y}_{i t}\), the within transformation. If you would prefer an algebraic argument, let \(d_{i}\) be a vector of \(N\) dummy variables where the \(i^{t h}\) element indicates the \(i^{t h}\) individual. Thus the \(i^{t h}\) element of \(d_{i}\) is 1 and the remaining elements are zero. Notice that \(u_{i}=d_{i}^{\prime} u\) and (17.32) equals \(Y_{i t}=d_{i}^{\prime} u+\varepsilon_{i t}\). This is a regression with the regressors \(d_{i}\) and coefficients \(u\). We can also write this in vector notation at the level of the individual as \(\boldsymbol{Y}_{i}=\mathbf{1}_{i} d_{i}^{\prime} u+\varepsilon_{i}\) or using full matrix notation as \(\boldsymbol{Y}=\boldsymbol{D} u+\boldsymbol{\varepsilon}\) where \(\boldsymbol{D}=\operatorname{diag}\left\{\mathbf{1}_{T_{1}}, \ldots, \mathbf{1}_{T_{N}}\right\}\).

The least squares estimate of \(u\) is

\[ \begin{aligned} \widehat{\boldsymbol{u}} &=\left(\boldsymbol{D}^{\prime} \boldsymbol{D}\right)^{-1}\left(\boldsymbol{D}^{\prime} \boldsymbol{Y}\right) \\ &=\operatorname{diag}\left(\mathbf{1}_{i}^{\prime} \mathbf{1}_{i}\right)^{-1}\left\{\mathbf{1}_{i}^{\prime} \boldsymbol{Y}_{i}\right\}_{i=1, \ldots, n} \\ &=\left\{\left(\mathbf{1}_{i}^{\prime} \mathbf{1}_{i}\right)^{-1} \mathbf{1}_{i}^{\prime} \boldsymbol{Y}_{i}\right\}_{i=1, \ldots, n} \\ &=\left\{\bar{Y}_{i}\right\}_{i=1, \ldots, n} . \end{aligned} \]

The least squares residuals are

\[ \widehat{\boldsymbol{\varepsilon}}=\left(\boldsymbol{I}_{n}-\boldsymbol{D}\left(\boldsymbol{D}^{\prime} \boldsymbol{D}\right)^{-1} \boldsymbol{D}^{\prime}\right) \boldsymbol{Y}=\dot{\boldsymbol{Y}} \]

as shown in (17.19). Thus the least squares residuals from the simple error-component model are the within transformed variables.

Now consider the error-component model with regressors, which can be written as

\[ Y_{i t}=X_{i t}^{\prime} \beta+d_{i}^{\prime} u+\varepsilon_{i t} \]

since \(u_{i}=d_{i}^{\prime} u\) as discussed above. In matrix notation

\[ \boldsymbol{Y}=\boldsymbol{X} \beta+\boldsymbol{D} u+\boldsymbol{\varepsilon} . \]

We consider estimation of \((\beta, u)\) by least squares and write the estimates as \(\boldsymbol{Y}=\boldsymbol{X} \widehat{\beta}+\boldsymbol{D} \widehat{u}+\widehat{\boldsymbol{\varepsilon}}\). We call this the dummy variable estimator of the fixed effects model.

By the Frisch-Waugh-Lovell Theorem (Theorem 3.5) the dummy variable estimator \(\widehat{\beta}\) and residuals \(\widehat{\boldsymbol{\varepsilon}}\) may be obtained by the least squares regression of the residuals from the regression of \(\boldsymbol{Y}\) on \(\boldsymbol{D}\) on the residuals from the regression of \(\boldsymbol{X}\) on \(\boldsymbol{D}\). We learned above that the residuals from the regression on \(\boldsymbol{D}\) are the within transformations. Thus the dummy variable estimator \(\widehat{\beta}\) and residuals \(\widehat{\boldsymbol{\varepsilon}}\) may be obtained from least squares regression of the within transformed \(\dot{Y}\) on the within transformed \(\dot{X}\). This is exactly the fixed effects estimator \(\widehat{\beta}_{\mathrm{fe}}\). Thus the dummy variable and fixed effects estimators of \(\beta\) are identical.

This is sufficiently important that we state this result as a theorem.

Theorem 17.1 The fixed effects estimator of \(\beta\) algebraically equals the dummy variable estimator of \(\beta\). The two estimators have the same residuals.

This may be the most important practical application of the Frisch-Waugh-Lovell Theorem. It shows that we can estimate the coefficients either by applying the within transformation or by inclusion of dummy variables (one for each individual in the sample). This is important because in some cases one approach is more convenient than the other and it is important to know that the two methods are algebraically equivalent.

When \(N\) is large it is advisable to use the within transformation rather than the dummy variable approach. This is because the latter requires considerably more computer memory. To see this consider the matrix \(\boldsymbol{D}\) in (17.34) in the balanced case. It has \(T N^{2}\) elements which must be created and stored in memory. When \(N\) is large this can be excessive. For example, if \(T=10\) and \(N=10,000\), the matrix \(\boldsymbol{D}\) has one billion elements! Whether or not a package can technically handle a matrix of this dimension depends on several particulars (system RAM, operating system, package version), but even if it can execute the calculation the computation time is slow. Hence for fixed effects estimation with large \(N\) it is recommended to use the within transformation rather than dummy variable regression.

The dummy variable formulation may add insight about how the fixed effects estimator achieves invariance to the fixed effects. Given the regression equation (17.34) we can write the least squares estimator of \(\beta\) using the residual regression formula:

\[ \begin{aligned} \widehat{\beta}_{\mathrm{fe}} &=\left(\boldsymbol{X}^{\prime} \boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{X}\right)^{-1}\left(\boldsymbol{X}^{\prime} \boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{Y}\right) \\ &=\left(\boldsymbol{X}^{\prime} \boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{X}\right)^{-1}\left(\boldsymbol{X}^{\prime} \boldsymbol{M}_{\boldsymbol{D}}(\boldsymbol{X} \beta+\boldsymbol{D} u+\boldsymbol{\varepsilon})\right) \\ &=\beta+\left(\boldsymbol{X}^{\prime} \boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{X}\right)^{-1}\left(\boldsymbol{X}^{\prime} \boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{\varepsilon}\right) \end{aligned} \]

since \(\boldsymbol{M}_{\boldsymbol{D}} \boldsymbol{D}=0\). The expression (17.35) is free of the vector \(u\) and thus \(\widehat{\beta}_{\mathrm{fe}}\) is invariant to \(u\). This is another demonstration that the fixed effects estimator is invariant to the actual values of the fixed effects, and thus its statistical properties do not rely on assumptions about \(u_{i}\).

17.12 Fixed Effects Covariance Matrix Estimation

First consider estimation of the classical covariance matrix \(\boldsymbol{V}_{\mathrm{fe}}^{0}\) as defined in (17.27). This is

\[ \widehat{\boldsymbol{V}}_{\mathrm{fe}}^{0}=\widehat{\sigma}_{\varepsilon}^{2}\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1} \]

with

\[ \widehat{\sigma}_{\varepsilon}^{2}=\frac{1}{n-N-k} \sum_{i=1}^{n} \sum_{t \in S_{i}} \widehat{\varepsilon}_{i t}^{2}=\frac{1}{n-N-k} \sum_{i=1}^{n} \widehat{\boldsymbol{\varepsilon}}_{i} \widehat{\boldsymbol{\varepsilon}}_{i} . \]

The \(N+k\) degree of freedom adjustment is motivated by the dummy variable representation. You can verify that \(\widehat{\sigma}_{\varepsilon}^{2}\) is unbiased for \(\sigma_{\varepsilon}^{2}\) under assumptions (17.18), (17.25) and (17.26). See Exercise 17.8.

Notice that the assumptions (17.18), (17.25), and (17.26) are identical to (17.5)-(17.7) of Assumption 17.1. The assumptions (17.8)-(17.10) are not needed. Thus the fixed effect model weakens the random effects model by eliminating the assumptions on \(u_{i}\) but retaining those on \(\varepsilon_{i t}\).

The classical covariance matrix estimator (17.36) for the fixed effects estimator is valid when the errors \(\varepsilon_{i t}\) are homoskedastic and serially uncorrelated but is invalid otherwise. A covariance matrix estimator which allows \(\varepsilon_{i t}\) to be heteroskedastic and serially correlated across \(t\) is the cluster-robust covariance matrix estimator, clustered by individual

\[ \widehat{\boldsymbol{V}}_{\mathrm{fe}}^{\text {cluster }}=\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \widehat{\boldsymbol{\varepsilon}}_{i} \widehat{\boldsymbol{\varepsilon}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1} \]

where \(\widehat{\boldsymbol{\varepsilon}}_{i}\) as the fixed effects residuals as defined in (17.23). (17.38) was first proposed by Arellano (1987). As in (4.55) \(\widehat{V}_{\text {fe }}^{\text {cluster }}\) can be multiplied by a degree-of-freedom adjustment. The adjustment recommended by the theory of C. Hansen (2007) is

\[ \widehat{\boldsymbol{V}}_{\mathrm{fe}}^{\text {cluster }}=\left(\frac{N}{N-1}\right)\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \widehat{\boldsymbol{\varepsilon}}_{i} \widehat{\boldsymbol{\varepsilon}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1} \]

and that corresponding to \((4.55)\) is

\[ \widehat{\boldsymbol{V}}_{\mathrm{fe}}^{\text {cluster }}=\left(\frac{n-1}{n-N-k}\right)\left(\frac{N}{N-1}\right)\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \widehat{\boldsymbol{\varepsilon}}_{i} \widehat{\boldsymbol{\varepsilon}}_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1} \text {. } \]

These estimators are convenient because they are simple to apply and allow for unbalanced panels.

In typical micropanel applications \(N\) is very large and \(k\) is modest. Thus the adjustment in (17.39) is minor while that in (17.40) is approximately \(\bar{T} /(\bar{T}-1)\) where \(\bar{T}=n / N\) is the average number of time periods per individual. When \(\bar{T}\) is small this can be a very large adjustment. Hence the choice between (17.38), (17.39), and (17.40) can be substantial.

To understand if the degree of freedom adjustment in (17.40) is appropriate, consider the simplified setting where the residuals are constructed with the true \(\beta\) but estimated fixed effects \(u_{i}\). This is a useful approximation since the number of estimated slope coefficients \(\beta\) is small relative to the sample size \(n\). Then \(\widehat{\boldsymbol{\varepsilon}}_{i}=\dot{\boldsymbol{\varepsilon}}_{i}=\boldsymbol{M}_{i} \boldsymbol{\varepsilon}_{i}\) so \(\dot{\boldsymbol{X}}_{i}^{\prime} \widehat{\boldsymbol{\varepsilon}}_{i}=\dot{\boldsymbol{X}}_{i}^{\prime} \boldsymbol{\varepsilon}_{i}\) and (17.38) equals

\[ \widehat{\boldsymbol{V}}_{\mathrm{fe}}^{\text {cluster }}=\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1}\left(\sum_{i=1}^{N} \dot{\boldsymbol{X}}_{i}^{\prime} \varepsilon_{i} \varepsilon_{i}^{\prime} \dot{\boldsymbol{X}}_{i}\right)\left(\dot{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)^{-1} \]

which is the idealized estimator with the true errors rather than the residuals. Since \(\mathbb{E}\left[\varepsilon_{i} \varepsilon_{i}^{\prime} \mid \boldsymbol{X}_{i}\right]=\Sigma_{i}\) it follows that \(\mathbb{E}\left[\widehat{\boldsymbol{V}}_{\mathrm{fe}}^{\text {cluster }} \mid \boldsymbol{X}\right]=\boldsymbol{V}_{\mathrm{fe}}\) and \(\widehat{\boldsymbol{V}}_{\mathrm{fe}}^{\text {cluster }}\) is unbiased for \(\boldsymbol{V}_{\mathrm{fe}}\) ! Thus no degree of freedom adjustment is required. This is despite the fact that \(N\) fixed effects have been estimated. While this analysis concerns the idealized case where the residuals have been constructed with the true coefficients \(\beta\) so does not translate into a direct recommendation for the feasible estimator, it still suggests that the strong ad hoc adjustment in (17.40) is unwarranted.

This (crude) analysis suggests that for the cluster robust covariance estimator for fixed effects regression the adjustment recommended by C. Hansen (17.39) is the most appropriate. It is typically well approximated by the unadjusted estimator (17.38). Based on current theory there is no justification for the ad hoc adjustment (17.40). The main argument for the latter is that it produces the largest standard errors and is thus the most conservative choice.

In current practice the estimators (17.38) and (17.40) are the most commonly used covariance matrix estimators for fixed effects estimation.

In Sections \(17.22\) and \(17.23\) we discuss covariance matrix estimation under heteroskedasticity but no serial correlation.

To illustrate, in Table \(17.2\) we present the fixed effect regression estimates of the investment model (17.3) in the third column with cluster-robust standard errors. The trading indicator \(T_{i}\) and the industry dummies cannot be included as they are time-invariant. The point estimates are similar to the random effects estimates, though the coefficients on debt and cash flow increase in magnitude.

17.13 Fixed Effects Estimation in Stata

There are several methods to obtain the fixed effects estimator \(\widehat{\beta}_{\mathrm{fe}}\) in Stata.

The first method is dummy variable regression. This can be obtained by the Stata regress command, for example reg y \(\mathrm{x}\) , cluster(id) where id is the group (individual) identifier. In most cases, as discussed in Section 17.11, this is not recommended due to the excessive computer memory requirements and slow computation. If this command is done it may be useful to suppress display of the full list of coefficient estimates. To do so, type quietly reg y \(x\) , cluster(id) followed by estimates table, keep( \(x_{-}\)cons) be se. The second command will report the coefficient(s) on \(x\) only, not those on the index variable id. (Other statistics can be reported as well.) The second method is to manually create the within transformed variables as described in Section 17.8, and then use regress.

The third method is \(x t r e g ~ f e\) which is specifically written for panel data. This estimates the slope coefficients using the partialling-out approach. The default covariance matrix estimator is classical as defined in (17.36). The cluster-robust covariance matrix (17.38) can be obtained using the options vce(robust) or \(r\).

The fourth method is areg absorb (id). This command is an alternative implementation of partiallingout regression. The default covariance matrix estimator is the classical (17.36). The cluster-robust covariance matrix estimator (17.40) can be obtained using the cluster(id) option. The heteroskedasticityrobust covariance matrix is obtained when \(\mathrm{r}\) or \(\mathrm{v} c e\) (robust) is specified but this is not recommended unless \(T_{i}\) is large as will be discussed in Section \(17.22\).

An important difference between the Stata xtreg and areg commands is that they implement different cluster-robust covariance matrix estimators: (17.38) in the case of xtreg and (17.40) in the case of areg. As discussed in the previous section the adjustment used by areg is ad hoc and not well-justified but produces the largest and hence most conservative standard errors.

Another difference between the commands is how they report the equation \(R^{2}\). This difference can be huge and stems from the fact that they are estimating distinct population counter-parts. Full dummy variable regression and the areg command calculate \(R^{2}\) the same way: the squared correlation between \(Y_{i t}\) and the fitted regression with all predictors including the individual dummy variables. The \(x t r e g ~ f e\) command reports three values for \(R^{2}\) : within, between, and overall. The “within” \(R^{2}\) is identical to what is obtained from a second stage regression using the within transformed variables. (The second method described above.) The “overall” \(R^{2}\) is the squared correlation between \(Y_{i t}\) and the fitted regression excluding the individual effects.

Which \(R^{2}\) should be reported? The answer depends on the baseline model before regressors are added. If we view the baseline as an individual-specific mean, then the within calculation is appropriate. If the baseline is a single mean for all observations then the full regression (areg) calculation is appropriate. The latter (areg) calculation is typically much higher than the within calculation, as the fixed effects typically “explain” a large portion of the variance. In any event as there is not a single definition of \(R^{2}\) it is important to be explicit about the method if it is reported.

In current econometric practice both xtreg and areg are used, though areg appears to be the more popular choice. Since the latter typically produces a much higher value of \(R^{2}\), reported \(R^{2}\) values should be viewed skeptically unless their calculation method is documented by the author.

17.14 Between Estimator

The between estimator is calculated from the individual-mean equation (17.20)

\[ \bar{Y}_{i}=\bar{X}_{i}^{\prime} \beta+u_{i}+\bar{\varepsilon}_{i} . \]

Estimation can be done at the level of individuals or at the level of observations. Least squares applied to (17.41) at the level of the \(N\) individuals is

\[ \widehat{\beta}_{\mathrm{be}}=\left(\sum_{i=1}^{N} \bar{X}_{i} \bar{X}_{i}^{\prime}\right)^{-1}\left(\sum_{i=1}^{N} \bar{X}_{i} \bar{Y}_{i}\right) . \]

Least squares applied to (17.41) at the level of observations is

\[ \widetilde{\beta}_{\mathrm{be}}=\left(\sum_{i=1}^{N} \sum_{t \in S_{i}} \bar{X}_{i} \bar{X}_{i}^{\prime}\right)^{-1}\left(\sum_{i=1}^{N} \sum_{t \in S_{i}} \bar{X}_{i} \bar{Y}_{i}\right)=\left(\sum_{i=1}^{N} T_{i} \bar{X}_{i} \bar{X}_{i}^{\prime}\right)^{-1}\left(\sum_{i=1}^{N} T_{i} \bar{X}_{i} \bar{Y}_{i}\right) . \]

In balanced panels \(\widetilde{\beta}_{\mathrm{be}}=\widehat{\beta}_{\text {be }}\) but they differ on unbalanced panels. \(\widetilde{\beta}_{\mathrm{be}}\) equals weighted least squares applied at the level of individuals with weight \(T_{i}\).

Under the random effects assumptions (Assumption 17.1) \(\widehat{\beta}_{\text {be }}\) is unbiased for \(\beta\) and has variance

\[ \boldsymbol{V}_{\mathrm{be}}=\operatorname{var}\left[\widehat{\beta}_{\mathrm{be}} \mid \boldsymbol{X}\right]=\left(\sum_{i=1}^{N} \bar{X}_{i} \bar{X}_{i}^{\prime}\right)^{-1}\left(\sum_{i=1}^{N} \bar{X}_{i} \bar{X}_{i}^{\prime} \sigma_{i}^{2}\right)\left(\sum_{i=1}^{N} \bar{X}_{i} \bar{X}_{i}^{\prime}\right)^{-1} \]

where

\[ \sigma_{i}^{2}=\operatorname{var}\left[u_{i}+\bar{\varepsilon}_{i}\right]=\sigma_{u}^{2}+\frac{\sigma_{\varepsilon}^{2}}{T_{i}} \]

is the variance of the error in (17.41). When the panel is balanced the variance formula simplifies to

\[ \boldsymbol{V}_{\mathrm{be}}=\operatorname{var}\left[\widehat{\beta}_{\mathrm{be}} \mid \boldsymbol{X}\right]=\left(\sum_{i=1}^{N} \bar{X}_{i} \bar{X}_{i}^{\prime}\right)^{-1}\left(\sigma_{u}^{2}+\frac{\sigma_{\varepsilon}^{2}}{T}\right) . \]

Under the random effects assumption the between estimator \(\widehat{\beta}_{\text {be }}\) is unbiased for \(\beta\) but is less efficient than the random effects estimator \(\widehat{\beta}_{\text {gls }}\). Consequently there seems little direct use for the between estimator in linear panel data applications.

Instead, its primary application is to construct an estimate of \(\sigma_{u}^{2}\). First, consider estimation of

\[ \sigma_{b}^{2}=\frac{1}{N} \sum_{i=1}^{N} \sigma_{i}^{2}=\sigma_{u}^{2}+\frac{1}{N} \sum_{i=1}^{N} \frac{\sigma_{\varepsilon}^{2}}{T_{i}}=\sigma_{u}^{2}+\frac{\sigma_{\varepsilon}^{2}}{\bar{T}} \]

where \(\bar{T}=N / \sum_{i=1}^{N} T_{i}^{-1}\) is the harmonic mean of \(T_{i}\). (In the case of a balanced panel \(\bar{T}=T\).) A natural estimator of \(\sigma_{b}^{2}\) is

\[ \widehat{\sigma}_{b}^{2}=\frac{1}{N-k} \sum_{i=1}^{N} \widehat{e}_{b i}^{2} . \]

where \(\widehat{e}_{b i}=\bar{Y}_{i}-\bar{X}_{i}^{\prime} \widehat{\beta}_{\text {be }}\) are the between residuals. (Either \(\widehat{\beta}_{\text {be }}\) or \(\widetilde{\beta}_{\text {be }}\) can be used.)

From the relation \(\sigma_{b}^{2}=\sigma_{u}^{2}+\sigma_{\varepsilon}^{2} / \bar{T}\) and (17.42) we can deduce an estimator for \(\sigma_{u}^{2}\). We have already described an estimator \(\widehat{\sigma}_{\varepsilon}^{2}\) for \(\sigma_{\varepsilon}^{2}\) in (17.37) for the fixed effects model. Since the fixed effects model holds under weaker conditions than the random effects model, \(\widehat{\sigma}_{\varepsilon}^{2}\) is valid for the latter as well. This suggests the following estimator for \(\sigma_{u}^{2}\)

\[ \widehat{\sigma}_{u}^{2}=\widehat{\sigma}_{b}^{2}-\frac{\widehat{\sigma}_{\varepsilon}^{2}}{\bar{T}} . \]

To summarize, the fixed effect estimator is used for \(\widehat{\sigma}_{\varepsilon}^{2}\), the between estimator for \(\widehat{\sigma}_{b}^{2}\), and \(\widehat{\sigma}_{u}^{2}\) is constructed from the two.

It is possible for (17.43) to be negative. It is typical to use the constrained estimator

\[ \widehat{\sigma}_{u}^{2}=\max \left[0, \widehat{\sigma}_{b}^{2}-\frac{\widehat{\sigma}_{\varepsilon}^{2}}{\bar{T}}\right] . \]

(17.44) is the most common estimator for \(\sigma_{u}^{2}\) in the random effects model.

The between estimator \(\widehat{\beta}_{\text {be }}\) can be obtained using the Stata command xtreg be. The estimator \(\widetilde{\beta}_{\text {be }}\) can be obtained by xtreg be wls.

17.15 Feasible GLS

The random effects estimator can be written as

\[ \widehat{\beta}_{\mathrm{re}}=\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{X}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \boldsymbol{X}_{i}^{\prime} \Omega_{i}^{-1} \boldsymbol{Y}_{i}\right)=\left(\sum_{i=1}^{N} \widetilde{\boldsymbol{X}}_{i}^{\prime} \widetilde{\boldsymbol{X}}_{i}\right)^{-1}\left(\sum_{i=1}^{N} \widetilde{\boldsymbol{X}}_{i}^{\prime} \widetilde{\boldsymbol{Y}}_{i}\right) \]

where \(\widetilde{\boldsymbol{X}}_{i}=\Omega_{i}^{-1 / 2} \boldsymbol{X}_{i}\) and \(\widetilde{\boldsymbol{Y}}_{i}=\Omega_{i}^{-1 / 2} \boldsymbol{Y}_{i}\). It is instructive to study these transformations.

Define \(\boldsymbol{P}_{i}=\mathbf{1}_{i}\left(\mathbf{1}_{i}^{\prime} \mathbf{1}_{i}\right)^{-1} \mathbf{1}_{i}^{\prime}\) so that \(\boldsymbol{M}_{i}=\boldsymbol{I}_{i}-\boldsymbol{P}_{i}\). Thus while \(\boldsymbol{M}_{i}\) is the within operator, \(\boldsymbol{P}_{i}\) can be called the individual-mean operator since \(\boldsymbol{P}_{i} \boldsymbol{Y}_{i}=\mathbf{1}_{i} \bar{Y}_{i}\). We can write

\[ \Omega_{i}=\boldsymbol{I}_{i}+\mathbf{1}_{i} \mathbf{1}_{i}^{\prime} \sigma_{u}^{2} / \sigma_{\varepsilon}^{2}=\boldsymbol{I}_{i}+\frac{T_{i} \sigma_{u}^{2}}{\sigma_{\varepsilon}^{2}} \boldsymbol{P}_{i}=\boldsymbol{M}_{i}+\rho_{i}^{-2} \boldsymbol{P}_{i} \]

where

\[ \rho_{i}=\frac{\sigma_{\varepsilon}}{\sqrt{\sigma_{\varepsilon}^{2}+T_{i} \sigma_{u}^{2}}} . \]

Since the matrices \(\boldsymbol{M}_{i}\) and \(\boldsymbol{P}_{i}\) are idempotent and orthogonal we find that \(\Omega_{i}^{-1}=\boldsymbol{M}_{i}+\rho_{i}^{2} \boldsymbol{P}_{i}\) and

\[ \Omega_{i}^{-1 / 2}=\boldsymbol{M}_{i}+\rho_{i} \boldsymbol{P}_{i}=\boldsymbol{I}_{i}-\left(1-\rho_{i}\right) \boldsymbol{P}_{i} . \]

Therefore the transformation used by the GLS estimator is

\[ \tilde{\boldsymbol{Y}}_{i}=\left(\boldsymbol{I}_{i}-\left(1-\rho_{i}\right) \boldsymbol{P}_{i}\right) \boldsymbol{Y}_{i}=\boldsymbol{Y}_{i}-\left(1-\rho_{i}\right) \mathbf{1}_{i} \bar{Y}_{i} \]

which is a partial within transformation.

The transformation as written depends on \(\rho_{i}\) which is unknown. It can be replaced by the estimator

\[ \widehat{\rho}_{i}=\frac{\widehat{\sigma}_{\varepsilon}}{\sqrt{\widehat{\sigma}_{\varepsilon}^{2}+T_{i} \widehat{\sigma}_{u}^{2}}} \]

where the estimators \(\widehat{\sigma}_{\varepsilon}^{2}\) and \(\widehat{\sigma}_{u}^{2}\) are given in (17.37) and (17.44). We obtain the feasible transformations

\[ \widetilde{\boldsymbol{Y}}_{i}=\boldsymbol{Y}_{i}-\left(1-\widehat{\rho}_{i}\right) \mathbf{1}_{i} \bar{Y}_{i} \]

and

\[ \widetilde{\boldsymbol{X}}_{i}=\boldsymbol{X}_{i}-\left(1-\widehat{\rho}_{i}\right) \mathbf{1}_{i} \bar{X}_{i}^{\prime} . \]

The feasible random effects estimator is (17.45) using (17.49) and (17.50).

In the previous section we noted that it is possible for \(\widehat{\sigma}_{u}^{2}=0\). In this case \(\widehat{\rho}_{i}=1\) and \(\widehat{\beta}_{\text {re }}=\widehat{\beta}_{\text {pool }}\).

What this shows is the following. The random effects estimator (17.45) is least squares applied to the transformed variables \(\widetilde{\boldsymbol{X}}_{i}\) and \(\widetilde{\boldsymbol{Y}}_{i}\) defined in (17.50) and (17.49). When \(\widehat{\rho}_{i}=0\) these are the within transformations, so \(\widetilde{\boldsymbol{X}}_{i}=\dot{\boldsymbol{X}}_{i}, \widetilde{\boldsymbol{Y}}_{i}=\dot{\boldsymbol{Y}}_{i}\), and \(\widehat{\beta}_{\mathrm{re}}=\widehat{\beta}_{\mathrm{fe}}\) is the fixed effects estimator. When \(\widehat{\rho}_{i}=1\) the data are untransformed \(\widetilde{\boldsymbol{X}}_{i}=\boldsymbol{X}_{i}, \widetilde{\boldsymbol{Y}}_{i}=\boldsymbol{Y}_{i}\), and \(\widehat{\beta}_{\mathrm{re}}=\widehat{\beta}_{\text {pool }}\) is the pooled estimator. In general, \(\widetilde{\boldsymbol{X}}_{i}\) and \(\widetilde{\boldsymbol{Y}}_{i}\) can be viewed as partial within transformations.

Recalling the definition \(\widehat{\rho}_{i}=\widehat{\sigma}_{\varepsilon} / \sqrt{\widehat{\sigma}_{\varepsilon}^{2}+T_{i} \widehat{\sigma}_{u}^{2}}\) we see that when the idiosyncratic error variance \(\widehat{\sigma}_{\varepsilon}^{2}\) is large relative to \(T_{i} \widehat{\sigma}_{u}^{2}\) then \(\widehat{\rho}_{i} \approx 1\) and \(\widehat{\beta}_{\text {re }} \approx \widehat{\beta}_{\text {pool. }}\). Thus when the variance estimates suggest that the individual effect is relatively small the random effect estimator simplifies to the pooled estimator. On the other hand when the individual effect error variance \(\widehat{\sigma}_{u}^{2}\) is large relative to \(\widehat{\sigma}_{\varepsilon}^{2}\) then \(\widehat{\rho}_{i} \approx 0\) and \(\widehat{\beta}_{\mathrm{re}} \approx \widehat{\beta}_{\mathrm{fe}}\). Thus when the variance estimates suggest that the individual effect is relatively large the random effect estimator is close to the fixed effects estimator.

17.16 Intercept in Fixed Effects Regression

The fixed effect estimator does not apply to any regressor which is time-invariant for all individuals. This includes an intercept. Yet some authors and packages (e.g. Amemiya (1971) and xtreg in Stata) report an intercept. To see how to construct an estimator of an intercept take the components regression equation adding an explicit intercept

\[ Y_{i t}=\alpha+X_{i t}^{\prime} \beta+u_{i}+\varepsilon_{i t} . \]

We have already discussed estimation of \(\beta\) by \(\widehat{\beta}_{\mathrm{fe}}\). Replacing \(\beta\) in this equation with \(\widehat{\beta}_{\mathrm{fe}}\) and then estimating \(\alpha\) by least squares, we obtain

\[ \widehat{\alpha}_{\mathrm{fe}}=\bar{Y}-\bar{X}^{\prime} \widehat{\beta}_{\mathrm{fe}} \]

where \(\bar{Y}\) and \(\bar{X}\) are averages from the full sample. This is the estimator reported by xtreg.

17.17 Estimation of Fixed Effects

For most applications researchers are interested in the coefficients \(\beta\) not the fixed effects \(u_{i}\). But in some cases the fixed effects themselves are interesting. This arises when we want to measure the distribution of \(u_{i}\) to understand its heterogeneity. It also arises in the context of prediction. As discussed in Section \(17.11\) the fixed effects estimate \(\widehat{u}\) is obtained by least squares applied to the regression (17.33). To find their solution, replace \(\beta\) in (17.33) with the least squares minimizer \(\widehat{\beta}_{\mathrm{fe}}\) and apply least squares. Since this is the individual-specific intercept the solution is

\[ \widehat{u}_{i}=\frac{1}{T_{i}} \sum_{t \in S_{i}}\left(Y_{i t}-X_{i t}^{\prime} \widehat{\beta}_{\mathrm{fe}}\right)=\bar{Y}_{i}-\bar{X}_{i}^{\prime} \widehat{\beta}_{\mathrm{fe}} . \]

Alternatively, using (17.34) this is

\[ \begin{aligned} \widehat{u} &=\left(\boldsymbol{D}^{\prime} \boldsymbol{D}\right)^{-1} \boldsymbol{D}^{\prime}\left(\boldsymbol{Y}-\boldsymbol{X} \widehat{\beta}_{\mathrm{fe}}\right) \\ &=\operatorname{diag}\left\{T_{i}^{-1}\right\} \sum_{i=1}^{N} d_{i} \mathbf{1}_{i}^{\prime}\left(\boldsymbol{Y}_{i}-\boldsymbol{X}_{i} \widehat{\beta}_{\mathrm{fe}}\right) \\ &=\sum_{i=1}^{N} d_{i}\left(\bar{Y}_{i}-\bar{X}_{i}^{\prime} \widehat{\beta}_{\mathrm{fe}}\right) \\ &=\left(\widehat{u}_{1}, \ldots, \widehat{u}_{N}\right)^{\prime} \end{aligned} \]

Thus the least squares estimates of the fixed effects can be obtained from the individual-specific means and does not require a regression with \(N+k\) regressors.

If an intercept has been estimated (as discussed in the previous section) it should be subtracted from (17.51). In this case the estimated fixed effects are

\[ \widehat{u}_{i}=\bar{Y}_{i}-\bar{X}_{i}^{\prime} \widehat{\beta}_{\mathrm{fe}}-\widehat{\alpha}_{\mathrm{fe}} \]

With either estimator when the number of time series observations \(T_{i}\) is small \(\widehat{u}_{i}\) will be an imprecise estimator of \(u_{i}\). Thus calculations based on \(\widehat{u}_{i}\) should be interpreted cautiously.

The fixed effects (17.52) may be obtained in Stata after ivreg, fe using the predict u command or after areg using the predict d command.

17.18 GMM Interpretation of Fixed Effects

We can also interpret the fixed effects estimator through the generalized method of moments.

Take the fixed effects model after applying the within transformation (17.21). We can view this as a system of \(T\) equations, one for each time period \(t\). This is a multivariate regression model. Using the notation of Chapter 11 define the \(T \times k T\) regressor matrix

\[ \overline{\boldsymbol{X}}_{i}=\left(\begin{array}{cccc} \dot{X}_{i 1}^{\prime} & 0 & \cdots & 0 \\ \vdots & \dot{X}_{i 2}^{\prime} & & \vdots \\ 0 & 0 & \cdots & \dot{X}_{i T}^{\prime} \end{array}\right) . \]

If we treat each time period as a separate equation we have the \(k T\) moment conditions

\[ \mathbb{E}\left[\overline{\boldsymbol{X}}_{i}^{\prime}\left(\dot{\boldsymbol{Y}}_{i}-\dot{\boldsymbol{X}}_{i} \beta\right)\right]=0 . \]

This is an overidentified system of equations when \(T \geq 3\) as there are \(k\) coefficients and \(k T\) moments. (However, the moments are collinear due to the within transformation. There are \(k(T-1)\) effective moments.) Interpreting this model in the context of multivariate regression, overidentification is achieved by the restriction that the coefficient vector \(\beta\) is constant across time periods.

This model can be interpreted as a regression of \(\dot{\boldsymbol{Y}}_{i}\) on \(\dot{\boldsymbol{X}}_{i}\) using the instruments \(\overline{\boldsymbol{X}}_{i}\). The 2SLS estimator using matrix notation is

\[ \widehat{\beta}=\left(\left(\dot{\boldsymbol{X}}^{\prime} \overline{\boldsymbol{X}}\right)\left(\overline{\boldsymbol{X}}^{\prime} \overline{\boldsymbol{X}}\right)^{-1}\left(\overline{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}\right)\right)^{-1}\left(\left(\dot{\boldsymbol{X}}^{\prime} \overline{\boldsymbol{X}}\right)\left(\overline{\boldsymbol{X}}^{\prime} \overline{\boldsymbol{X}}\right)^{-1}\left(\overline{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{Y}}\right)\right) \]

Notice that

\[ \begin{aligned} & \overline{\boldsymbol{X}}^{\prime} \overline{\boldsymbol{X}}=\sum_{i=1}^{n}\left(\begin{array}{cccc}\dot{X}_{i 1} & 0 & \cdots & 0 \\\vdots & \dot{X}_{i 2} & & \vdots \\0 & 0 & \cdots & \dot{X}_{i T}\end{array}\right)\left(\begin{array}{cccc}\dot{X}_{i 1}^{\prime} & 0 & \cdots & 0 \\\vdots & \dot{X}_{i 2}^{\prime} & & \vdots \\0 & 0 & \cdots & \dot{X}_{i T}^{\prime}\end{array}\right) \\ & =\left(\begin{array}{cccc}\sum_{i=1}^{n} \dot{X}_{i 1} \dot{X}_{i 1}^{\prime} & 0 & \cdots & 0 \\\vdots & \sum_{i=1}^{n} \dot{X}_{i 2} \dot{X}_{i 2}^{\prime} & & \vdots \\0 & 0 & \cdots & \sum_{i=1}^{n} \dot{X}_{i T} \dot{X}_{i T}^{\prime}\end{array}\right) \text {, } \\ & \overline{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{X}}=\left(\begin{array}{c}\sum_{i=1}^{n} \dot{X}_{i 1} \dot{X}_{i 1}^{\prime} \\\vdots \\\sum_{i=1}^{n} \dot{X}_{i T} \dot{X}_{i T}^{\prime}\end{array}\right) \text {, } \end{aligned} \]

and

\[ \overline{\boldsymbol{X}}^{\prime} \dot{\boldsymbol{Y}}=\left(\begin{array}{c} \sum_{i=1}^{n} \dot{X}_{i 1} \dot{Y}_{i 1} \\ \vdots \\ \sum_{i=1}^{n} \dot{X}_{i T} \dot{Y}_{i T} \end{array}\right) \text {. } \]

Thus the 2SLS estimator simplifies to

\[ \begin{aligned} \widehat{\beta}_{2 \mathrm{sls}} &=\left(\sum_{t=1}^{T}\left(\sum_{i=1}^{n} \dot{X}_{i t} \dot{X}_{i t}^{\prime}\right)\left(\sum_{i=1}^{n} \dot{X}_{i t} \dot{X}_{i t}^{\prime}\right)^{-1}\left(\sum_{i=1}^{n} \dot{X}_{i t} \dot{X}_{i t}^{\prime}\right)\right)^{-1} \\ & \times\left(\sum_{t=1}^{T}\left(\sum_{i=1}^{n} \dot{X}_{i t} \dot{X}_{i t}^{\prime}\right)\left(\sum_{i=1}^{n} \dot{X}_{i t} \dot{X}_{i t}^{\prime}\right)^{-1}\left(\sum_{i=1}^{n} \dot{X}_{i t} \dot{Y}_{i t}\right)\right) \\ &=\left(\sum_{t=1}^{T} \sum_{i=1}^{n} \dot{X}_{i t} \dot{X}_{i t}^{\prime}\right)^{-1}\left(\sum_{t=1}^{T} \sum_{i=1}^{n} \dot{X}_{i t} \dot{Y}_{i t}\right) \\ &=\widehat{\beta}_{\mathrm{fe}} \end{aligned} \]

the fixed effects estimator!

This shows that if we treat each time period as a separate equation with its separate moment equation so that the system is over-identified, and then estimate by GMM using the 2SLS weight matrix, the resulting GMM estimator equals the simple fixed effects estimator. There is no change by adding the additional moment conditions.